Projects

Technical work spanning quantitative finance, mathematical modeling, and software development.

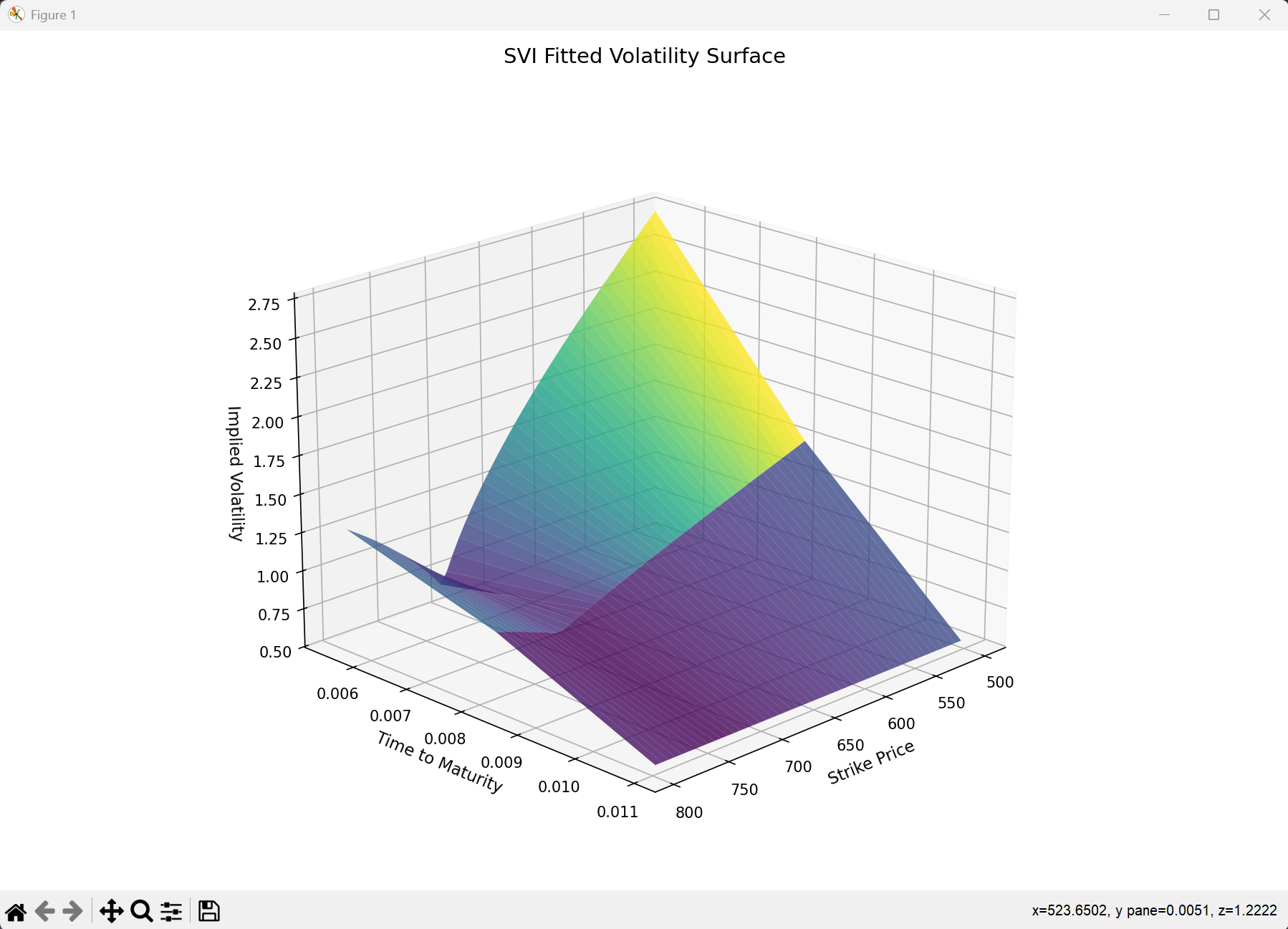

Arbitrage-Free Volatility Surface

ActiveProduction-grade Python toolkit for computing implied volatilities, enforcing no-arbitrage constraints, fitting SVI models, and calibrating Heston stochastic volatility models to market data. Features robust IV computation, 3D surface visualization, and comprehensive testing.

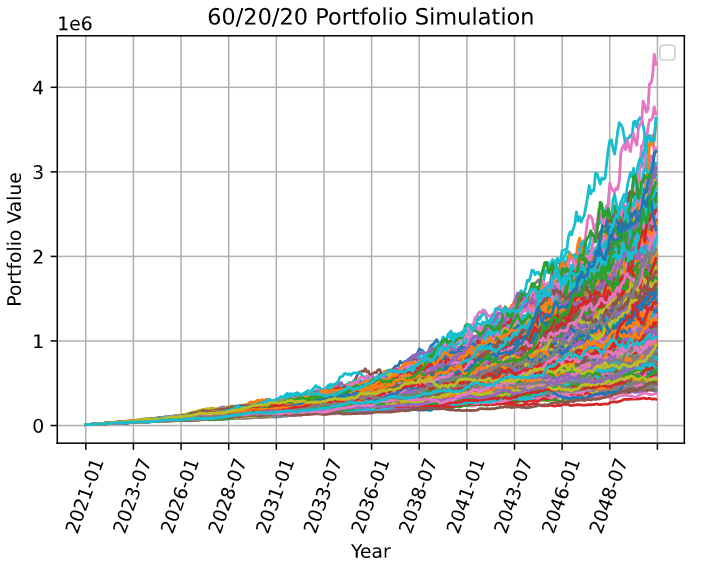

Monte Carlo Variance Reduction

In ProgressResearch project exploring advanced variance reduction techniques for Monte Carlo simulations. Investigating control variates, importance sampling, and antithetic variables to improve computational efficiency in financial modeling.

Physics-Informed FX Currency Network

In ProgressApplying physics-informed neural networks to model foreign exchange currency relationships. Incorporating structural constraints and domain knowledge to improve prediction accuracy and interpretability in currency markets.

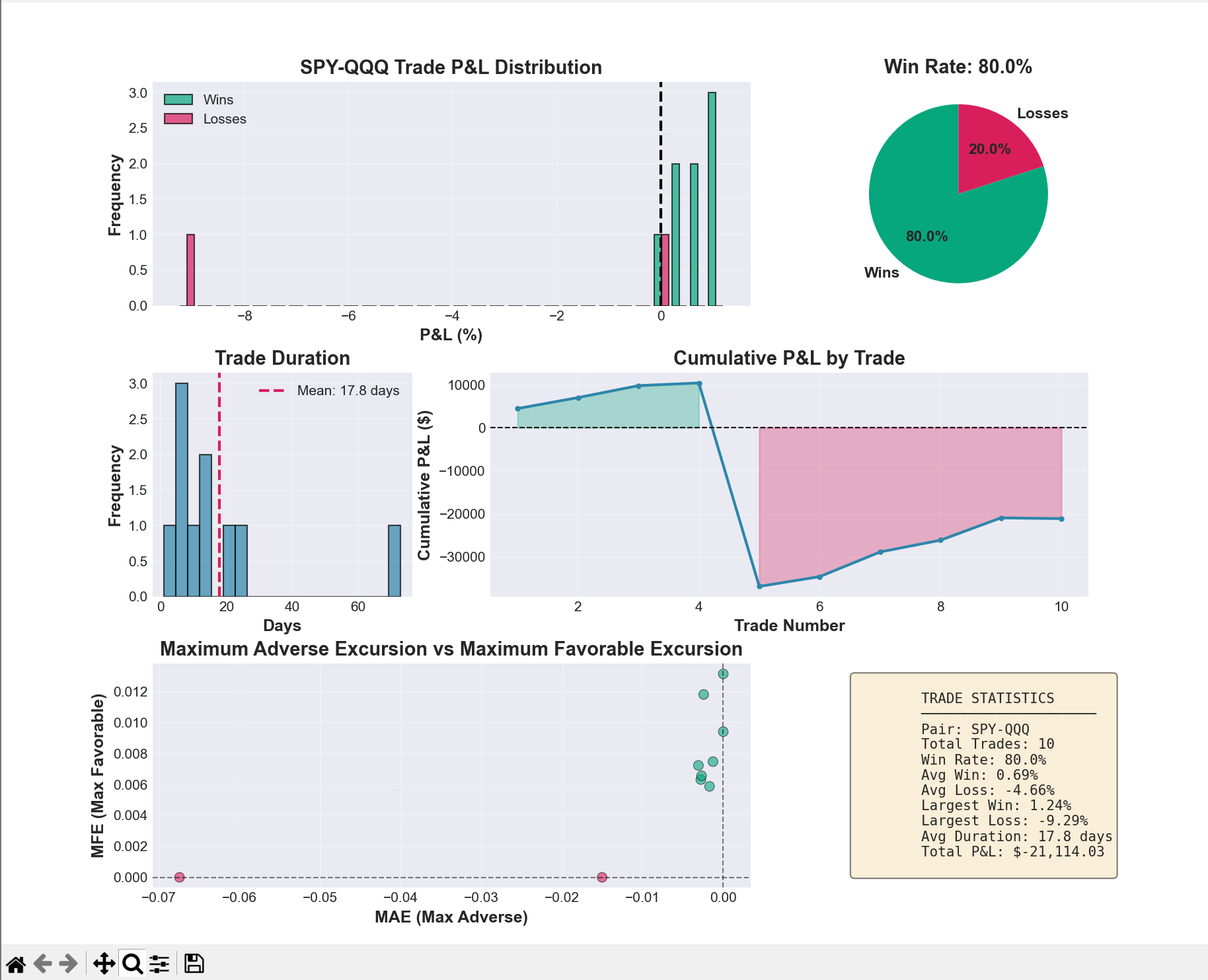

Impact of Corporate Changes on Market Volatility

PublishedPublished research analyzing how corporate events and leadership changes affect market volatility and returns. Conducted for AlgoGators quantitative hedge fund with plans to expand the study with additional market metrics.

CHIV LLC

Launching Feb 2026Founded and developing CHIV, a startup project in stealth mode. Six months in development with public launch scheduled for February 2026. Building innovative solutions at the intersection of technology and finance.